High-end furniture maker RH (NYSE:RH)�-- formerly Restoration Hardware -- continues to defy skeptics. The company's most recent earnings report propelled the stock higher by more than 30% in a single day. Since hitting a low in February 2017, shares are up a whopping 450% as of this writing.

It has been easy to make a bearish case against RH in recent years considering a challenging brick-and-mortar retail environment and the company's burdensome debt. But short-sellers look woefully unstylish at the moment. Here are three reasons this stock is soaring.

RH data by YCharts.�

1. The business is humming along

First off, RH is getting things done at an operational level. It is successfully selling high-end furnishings both in stores and online -- what's called an "omnichannel" strategy in the retail world. In 2017, for example, transactions in stores accounted for 56% of total sales, and the remainder were from "direct business" through its catalog and website.

This balanced approach is critical to compete with purely online, low-cost heavyweights like Amazon.com and Wayfair in the furnishings space. Customers searching for sofas that cost thousands of dollars want to see and feel the product in person, but they also want to be able to customize their exact purchase through an easy-to-use website. RH has done an enviable job of meeting their needs.

An added benefit is that optimizing for a specific sales channel has not consumed the company's salesforce. Instead, CEO Gary G. Friedman has emphasized a product-first strategy, with the various channels -- brick-and-mortar, online, and catalog -- being equally capable of facilitating and closing the sales of those products. This is described in the company's 2017 annual report as follows: "We encourage our customers to shop across our channels and have aligned our business and internal organization to be channel agnostic."

Two things are particularly impressive about RH's channel shift: (1) The company has prevented cannibalization such that sales have continued to grow at a steady clip over the last eight years and�(2) the transition has not created excessive marketing and administrative expenses as RH dialed in its omnichannel approach.

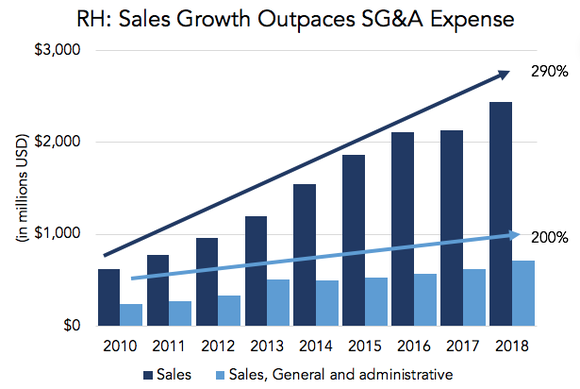

The following chart shows why the market's impressed with RH's recent sales and marketing accomplishments. In eight years, sales have grown 290% versus a comparably slower increase in sales, general, and administrative expenses of 200%.

Data source: Morningstar data, author's calculations.

Overall, this trend has been a significant contributor to the recent quarterly earnings surprises (see here, here, and here), and is illustrative of the operational execution that has propelled RH's stock price higher.

2. The company is heavily buying back shares

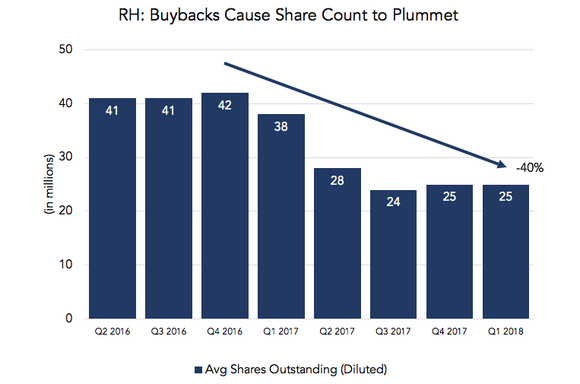

The second factor contributing to RH's rapidly growing stock price is a string of share buybacks executed by the company. These share repurchases are nothing to sneeze at: More than $1 billion of the company's capital has been dedicated to buying shares off the open market, which has led to a 40% reduction of shares outstanding since the fourth quarter of 2016.

The following chart shows the decline in outstanding stock, with the largest reduction taking place in 2017 when a $300 million and $700 million buyback were proposed, approved by the board, and executed:

Data source: Morningstar data, author's calculations.

With share buybacks, companies typically use excess cash on their balance sheets to "retire" shares, ideally at a point in time where leadership sees the company's stock as undervalued by the market. A share repurchase doesn't change the market capitalization of the company by itself, but it does entitle the remaining common shareholders to a bigger slice of the earnings pie. As a result, this can send the stock higher, as has been the case for RH.

RH's share repurchases look extremely savvy in retrospect, given the stock has soared since their execution. However, there are some legitimate reasons to question this move, especially considering the fact that RH is not sitting on a pile of cash and instead raised debt to effect the share repurchase. Discussing the merits of RH's share repurchase is a debate for another article, however, and it's a topic that's been well-covered by my Foolish colleague Brian Stoffel. As he points out, there are perfectly valid reasons to be skeptical of the CEO's incentives for propelling RH's stock price higher through leveraged share buybacks.

Despite the risk of added debt, the share repurchases have propelled the stock higher by boosting quarterly earnings per share, and they've also had an effect on the company's unique short-seller situation. This brings us to our final -- and perhaps most important -- driver of RH's recent share price run-up.

3. The short-sellers are getting squeezed big-time

The third reason RH's stock price has ballooned is due to a unique "short-squeeze" situation. A short-squeeze involves investors betting against a stock by borrowing shares in the expectation that the stock price will decrease in the future. If the stock price does not decrease, those short-sellers are in a losing position because they must purchase the shares at a higher price to return the ones they borrowed.

This is not only happening with RH's stock, but it's happening on an exaggerated level . RH, as a risky, debt-laden participant in the declining brick-and-mortar retail industry, has found itself heavily shorted, to the point where more than 60% of its shares outstanding were sold short in the middle of 2017. In the past two years, the average percent of shares outstanding short at RH has hovered around 35%, which is roughly where it stands today. Here's a look at that trend and how it compares at retail peers Williams-Sonoma�and The TJX Companies.

RH Percent of Shares Outstanding Short data by YCharts.

As you can see, there's a greater proportion of short-sellers tied to RH than to its peers. Investors are betting against RH's future in hopes that it will underperform. Ironically, as the opposite happens -- i.e., when RH posts better operational results (see point No. 1 above) and buys back shares (see No. 2 above) -- these catalysts push the stock higher and force short-sellers to decide whether they want to ride out their bet longer or close their position. If they do the latter, they must buy shares in the company to do so, which in turn pushes the stock even higher.There is a compounding effect at work here, and it doesn't end there. With RH, there aren't hundreds of millions of shares outstanding. There are roughly 25 million at RH, compared to 625 million at The TJX Companies. This is called a small "float." This can lead to a scarcity of sellers when the shorts need trading to take place, which can in turn force them to bid the price even higher. What ends up happening is an "infinity squeeze" is created when the unusual shortage of supply rockets a share price upward.It is one thing to see a stock price grow on strong earnings, but quite another for those results to be inflated by share repurchases and propelled beyond logic by the peculiar machinations of an infinity short squeeze. But this is what's happening at RH.

The takeaway for investors

With a track record of 450% stock price growth in less than two years, it's not surprising to see that there's something unusual happening here at RH, something that goes beyond the fundamentals of the business.

Yes, the company is performing well and adapting to change in the retail world, but it has also benefited from some risky bets where a large sum of debt was used to repurchase its own stock. Beyond that, it's seen external factors -- a high percentage of short-sellers -- contribute to the stock's meteoric rise as they get squeezed out of their position. RH has an impressive tailwind, but it's definitely not a stock for the faint of heart right now.

IBM mentors work with P-Tech engineering students.

IBM mentors work with P-Tech engineering students.  P-Tech graduate Janiel Richards meets with IBM CEO Ginni Rometty.

P-Tech graduate Janiel Richards meets with IBM CEO Ginni Rometty.